11:26 18.05.2026 •

11:26 18.05.2026 •

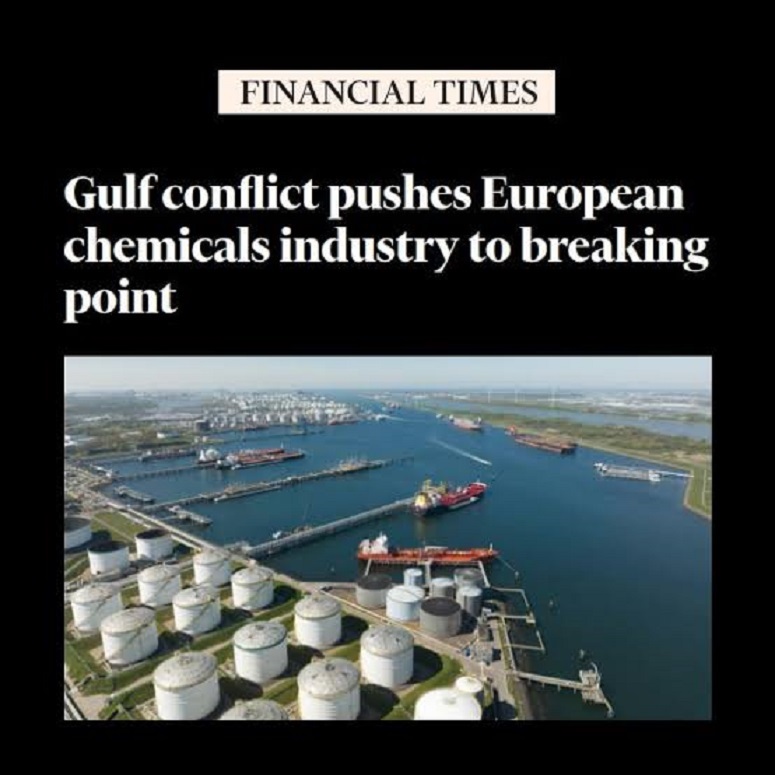

In the Port of Rotterdam, one of the world’s largest and most advanced chemical clusters is at a critical juncture. Smoke still billows across the skyline and tankers travel back and forth through the port, ferrying feedstock into vast drums that are linked to facilities by pipelines, ‘Financial Times’ writes.

But two of the cluster’s 10 companies have shut down plants in the past year as the European chemicals industry is buffeted by high energy prices, weak demand and intensifying competition from China.

While the Middle East conflict has offered something of a reprieve by disrupting Chinese plants that rely on feedstock from the Gulf, it has also pushed energy costs higher and stoked price volatility for critical inputs such as naphtha, with knock-on effects on downstream chemicals markets.

“Developments in the Middle East are pushing energy costs even higher, reinforcing how exposed the UK and Europe remain to external shocks,” said Peter Huntsman, chief executive of Huntsman Corporation, which operates sites across Europe, including Rotterdam.

Even if the crisis had helped some European producers, a peace deal could “bring all the problems back”, said James Hooper, senior analyst in chemicals at research firm Bernstein.

A return to “unprecedented” closures could risk a domino effect, according to Yvonne van der Laan, executive vice-president at US-listed chemicals group LyondellBasell. “This... takes the heart out of these integrated value chains,” she said. “When that starts to happen, it’s a matter of time before the entire ecosystem comes down.”

To add to the pain in Rotterdam, Mitsubishi said in February it would end construction of an advanced production unit for MXDA, a chemical intermediate used in high-performance coatings for ships, military equipment and other industrial applications.

Nor are the closures in Rotterdam a localised phenomenon.

Plant shutdowns across Europe have risen

Plant shutdowns across Europe have risen sixfold over the past four years, according to industry body Cefic, leading to the loss of almost a tenth of Europe’s production capacity and directly affecting about 20,000 jobs across the continent. Investment in Europe’s chemical sector fell more than 80 per cent last year.

The closures and falling investment threaten Europe’s ability to make the basic materials for modern life, from the chlorine used to purify drinking water to the phenols used in printed circuit boards.

The industry’s production facilities typically operate in clusters to take advantage of shared infrastructure, with material produced by one company often fed to a neighbour. The result is a symbiotic network of plants that rely upon one another for survival. The byproduct from one chemical reaction, useless to the company that made it, might be an essential feedstock for a neighbouring business.

In Rotterdam’s chlorine cluster, the closure of titanium dioxide maker Tronox’s facility and Westlake Corporation’s epoxy resin plant means there is less demand for chlorine, made by producer Nobian, which sits at the centre of the network.

If Nobian decides to close its facility, the local companies that had relied upon its material as feedstock will be forced to import the material, raising their costs and compounding their strains.

It is a problem replicated across the continent. The Port of Rotterdam’s chemical cluster is part of a constellation of sites that stretch across Europe, connected by pipeline. Rotterdam is linked to Antwerp, another major cluster, and the two supply Germany’s Rhine and Ruhr regions, the beating heart of Europe’s heavy industries, including its automotive sector.

Matthias Berninger, executive vice-president at pharmaceuticals group Bayer and a former German government minister, compared the problem to a Jenga tower. “What you see is that a whole lot of little wooden blocks have been taken out of the tower... At some point, this all comes crashing down.”

Many Chinese plants have declared force majeure as a result of the war, offering European producers a breather, but the bloc’s high energy costs and decision to phase out Russian gas supplies by 2027, coupled with an increasingly high carbon price, mean the fundamental issues are little changed.

“You can only do what you can do, really, which is pray”

A new report from credit insurer Atradius said it expected chemicals production in the EU and the UK to decrease by 2.2 per cent in 2026, 1.8 percentage points more than its prewar forecast in February.

Houston-based LyondellBasell said energy costs at its Rotterdam chemical facility were now three times higher than at its US sites and could double if the EU proceeds with a tightening of its flagship emissions trading scheme.

Politicians and industry executives are lobbying Brussels to ease its ETS when it comes up for review this summer. But few European chemicals executives are optimistic.

Although the EU chemicals sector ran a trade surplus of €31.3bn in the first 10 months of 2025, that was down by €7.3bn compared with the same period in 2024 and was solely driven by exports of speciality chemicals rather than commodity products critical to manufacturing, according to Cefic.

Huntsman said the continent had to choose whether it wanted to retain its industrial capability or “become a geriatric Disneyland, a large service-oriented economy where a lot of wealthy old people go tour castles”.

Jim Ratcliffe, chief executive of Ineos, told the FT that chemicals companies had few options left: “You can only do what you can do, really, which is pray.”

read more in our Telegram-channel https://t.me/The_International_Affairs